A narrative that persists in Africa today is that African countries are beholden to external debt servicing and in turn, African states lack policy space around social spending and other public investment. International financial institutions are the most cited culprit of this beholding, and indebted African countries are condoled as victims.

Fantu Cheru (2021), for instance, traces the story back to the 1980s and 1990s, arguing that “a new world order” took hold, characterized by big firms, conditional aid, and lending aimed at opening African markets and dismantling the African state of the 1960s and early 1970s. Similarly, world historical analyst, Fouad Makki, asserts that through the 1980s and 1990s, Africa was “subjected” to structural adjustment programs “designed to restructure Africa into a deregulated world economy” (Makki 2015, 125). He further laments that “African states were powerless . . . and unrestrained capital flows and the dismantling of national regulatory frameworks undermined what little economic sovereignty they had previously exercised” (Makki 2015, 137). Along similar lines, African governments cite debt servicing and international credit agency ratings as justification for continuing and deepening policies of austerity.

Contrary to these approaches, it is argued here that African elites have actively played a part in capitalist structural reforms, and these have been a success from the perspective of world elites, African elites included. The US, as world hegemon, with the support of other G7 countries, revitalized a faltering International Monetary Fund, in the early 1980s, to serve the needs of international banks and what was perceived as an impending financial failure in the capitalist world-economy. African elites contributed to maintaining the world capitalist structure at this time by shifting to externally oriented development similar to that of the colonial era, with a new twist: foreign credit combined with offshore transactions for the purpose of saving and investing capital. These choices, of African and other elites, are argued to occur within a world historical moment of what world systems analysts have formulated as crisis and chaos in the world system (Amin 1995), in a period of restructuring and financial expansion in the fourth (US) systemic cycle of accumulation (Arrighi 1994). Elite political choices have created the conditions for the African continent, and its peoples, to become a major locus for the maintenance of world financial and trade flows, albeit in shaky balance.

The discussion is organized in four parts. The first revisits historical discussions of international debt, drawing from critical, mainstream, and official perspectives produced or published between the 1980s and early 2000s. These accounts and analyses are, at best, little known and, at worst, lost in current discussions of debt and economic policy, particularly in Africa. The second part provides a theoretical overview of global material and financial expansion in world historical perspective. It elaborates how a massive supply of cheap credit became available, worldwide, by the early 1970s, and how and why this credit was amassed by African and other Majority World states. The third part focuses on the specific experience of the fourth (US) systemic cycle of accumulation in the African continent, elaborating on the agency of African elites circa 1960 to mid-1980. The fourth part offers a preliminary sketch of policy tendencies in Africa, from circa 1990 to the present. Rather than a comprehensive picture, it is proposed that this preliminary sketch is a framework through which the breadth of experiences in the 54 countries of Africa may be specified and historicized, while drawing links with the systemic forces discussed in the first three parts.

Demystifying Debt

In his 1995 essay, “Fifty Years Is Enough!”—named in the spirit of President Thomas Sankara’s 1987 speech—Samir Amin cited the 1993 International People’s Tribunal to Judge the G7 Tokyo Verdict by way of summarizing the critiques of “structural adjustment programs” made until then. The verdict was that, alongside continued growth of external debt, structural adjustment resulted in sharp rises in unemployment, falling remuneration levels, increased food dependency, grave deterioration of the environment, deterioration of healthcare, falling admissions to educational institutions, productive capacity declines, and the sabotage of democracy (as cited by Amin 1995). Amin’s critique of these critiques is that they were purely moral, lacking an analysis of world capitalism. In Amin’s words, “policies are accused of fostering poverty, as if the logic of the system had nothing to do with it” (1995, 10).

Amin (1995, 42) provides debt figures from the mid-1990s that hint at this logic: “The debt grew from $900 billion in 1982 to $1,500 trillion, of which half was expended on interest.” Though little spoken of today, these figures, and their meaning, were well known to the US elite in the 1980s. The 1986 Joint Economic Report notes:

The total debt of the nonoil developing countries rose from about 22 percent of their GDP in 1973 to 35 percent in 1983. In 1985, Lesser Development Country (LDC) debt was over $800 billion. The debt situation in Latin America is on the brink of renewed crisis. Debtor countries have covered their debt servicing costs only by going further into debt and by a rapid swing from trade deficit to trade surplus . . . their real debt burden is higher today than it was when the last “crisis” began in 1982. (Congress of the United States Joint Economic Committee 1986, 61)

Writing retrospectively on debt in Latin America, Ocampo (n.d., 14) notes that debt coefficients in the early 1980s were modest, amounting, on average, to below 30 percent of GDP and about double the value of exports. Ocampo underlines that after five to six years of “structural adjustment,” Latin America’s external debt coefficients doubled, and did not drop back to pre-crisis levels until the first decade of the 21st century.

Naming a part of what was at play in plain language, the Wall Street Journal put it like this in 1986:

Bank profits have grown steadily during the debt crisis, according to a report of the Joint Economic Committee of Congress . . . the Administration’s whole approach to the debt crisis has kept the banks solvent but it has sunk the debtor nations further in debt. (quoted in Bienefeld 2000, 535)

In a 1993 document of the International Council of Volunteer Agencies (ICVA), the Council’s General Secretary, Marcos Arruda, thus stated that the South had become “an exporter of capital to the North” while the debt crisis remained unresolved (as cited by Amin 1995, 11). Offering an academic discussion of Arruda’s view, in a journal article titled “Structural Adjustment: Debt Collection Device of Development Policy?,” Manfred Bienefeld (2000, 536) argued that the diffusion of structural adjustment programs “had more to do with power and leverage than with persuasion.” Bienefeld cites IMF studies of the 1980s to underline the ideological nature of IMF prescriptions that were termed “policies to restore development,” rather than the debt collection devices that they actually were. For example, a 1989 study by Feldman and co-authors acknowledged that “structural reforms now being considered in industrial countries are relatively minor compared to comprehensive stabilization-cum-liberalization programs” implemented in the South (Feldman et al. 1989, 7; as cited by Bienefeld 2000, 536).

In the US Congress 1986 Joint Economic Committee report, considerably more space is dedicated to discussing rising debt within the US than the third world debt crisis. In the third of 11 sections in the “Democratic Views” part of the report, titled “The Outlook for the Future,” a sub-section titled “The Great Debt” includes, among others, elaborations on “corporate debt,” “farm debt,” “public debt” and the associated current account deficit, “the thrift crisis,” and “the ticking time bomb of US financial structure” (Congress of the United States Joint Economic Committee 1986, 52–64). On the latter two, the report identified the extent of insolvency of the US banking sector, and the inability of state institutions to provide rescue. The detail is revealing and worth citing at length:

Barred by law from underwriting mutual funds or commercial paper, banks have been retaliating against Wall Street’s incursions by offering corporate clients liquidity in the form of commitments—to make loans, to buy or sell foreign currency, or to guarantee the obligations of a creditor. Banks can charge tidy fees for making these commitments and yet not set aside capital to back them, as they would loans. At the end of 1984, these “off-balance sheet liabilities” at the 15 largest banks totaled $930 billion, or about 8 percent more than their assets.

Deregulation has also created new competitive pressure in the thrift sector. Many states permit savings and loans virtual carte blanche in making investments, and the result has been a series of spectacular investment mistakes by institutions unprepared to handle such discretion in a highly competitive environment. High risk loan strategies underlie the crises at Financial Corporation of America in California, and the thrift crisis in both Ohio and Maryland.

Options for dealing with a large-scale problem in the financial system are limited. The GAO said that the cost of rescuing 434 insolvent institutions could be $15 billion to $20 billion. But the Federal Savings and Loan Insurance Corporation (FSLIC) now has only $2.6 billion it can use for this purpose. Federal Home Loan Bank Board officials have suggested that a means of augmenting the insurance fund would be to require the Federally insured thrifts to contribute 1 percent of their deposits to the FSLIC. But the GAO found that it would force an additional 159 thrifts into insolvency. (Congress of the United States Joint Economic Committee 1986, 63–64)

Rather than finding a solution to the mass of debt accumulated in the world economy as a whole—both within the largest country at the core of the system, the US, and in countries of the system’s periphery, Asia, Africa, Latin America and the Caribbean—the US elite opted to manage the crisis. Putting it in a word, Amin (1995, 42) described this “management” as “maintaining the world in a state of stagnation.” This was done, from the early 1980s, by perpetuating debt in the periphery via so-called structural adjustment, and inducing unemployment and underemployment at the core through increased interest rates and other measures.

Amin noted that the IMF was never given the power to adjust the structure of the US economy. This despite the fact that the US had become a debtor nation, as the Joint Economic Committee report specified, in the section titled “International Debt,” with an unmistaken tone of alarm:

A few short years ago, a discussion of the “world debt problem” would have involved only a discussion of the debt of the developing world. No longer. During 1985, the United States became a debtor nation for the first time in 68 years. Since then, we have been going into net foreign debt faster than any country in recorded history. Last year, we imported capital at the unprecedented rate of over 3 percent of GNP per year. At present rates, many estimate that we could accumulate a net foreign debt of over a trillion dollars by the mid-1990s. (Congress of the United States Joint Economic Committee 1986, 58)

By 1995, the US external debt had in fact reached 4.97 trillion USD (US Department of the Treasury 2013). Amin argued at the time that increased flows of foreign exchange from the periphery are what had allowed the system to maintain liberalized world trade and financial flows alongside the continued rise of the US’s current account deficit. In Amin’s (1995, 40) words, the US deficit “is large enough to absorb all of the surpluses of the developed regions . . . and it has drained the international market of capital that would otherwise have been available for other regions of the world.”

In 1995, Amin asked, “Is this type of management strong enough to last?” Answering the question, he conjectured that such management “can indeed be pursued successfully.” With regard to countries of the periphery, Amin (1995, 42) foresaw “grave regressive involution, of which the Fourth Worldization of Africa is simply the most extreme example.”

Some 20 years later, Ndikumana and Boyce’s (2021, 1) time series estimates of capital flight from Africa help confirm much of Amin’s conjecture. According to their findings, between 1970 and 2018, for the 30 African countries for which there are sufficient data, 2 trillion USD were lost to capital flight. The major forms of capital flight are misinvoicing of imports and exports, and transfers to offshore bank accounts by African government officials. 1 Estimating the stock of offshore wealth accumulated since the 1970s through capital flight at 2.4 trillion USD, Ndikumana and Boyce (2021, 1) stress this amount “far exceeds the $720 billion of external debt owed by this group of countries” as of 2018. Accounting for other inflows, including overseas development assistance, remittances, foreign direct investment, and portfolio investment, they assert that Africa is “a net creditor to the rest of the world,” to the tune of 1.6 trillion USD (Ndikumana and Boyce 2021, 7). Ndikumana and Boyce’s assertion echoes the 1993 statement of ICVA General Secretary Arruda, though with a somewhat narrower focus. Such a focus is justified given that today, African countries make up the vast majority of highly indebted nations; more specifically, 34 of 39 countries in the World Bank’s (2021) “highly indebted countries” (HIPC) list. 2

The view of Africa as a creditor in the world economy is the stark opposite of widespread views, both within Africa and beyond, that Africa is highly indebted and capital-scarce. African states have used this perception to continue policies of austerity, up to and including during the first two years of the global COVID-19 pandemic, marked, in much of the world, by an expansion of fiscal policy.

How to explain the choices and actions of African elites over the past 40 to 50 years? What follows is an analysis to help answer this question, within the context of what Giovanni Arrighi has theorized as the fourth (US) systemic cycle of accumulation.

Theoretical Overview: The Fourth (US) Systemic Cycle of Accumulation

Giovanni Arrighi (1994) traces four systemic cycles of accumulation over the longue durée of historical capitalism, each denoted by the leading, or hegemonic capitalist state of the time: the first (Genoese) systemic cycle, circa 1450–1640; the second (Dutch) cycle, circa 1640–1790; the third (British) cycle, circa 1790–1925; and the fourth (US) cycle, circa 1925–present. In each cycle, Arrighi historicizes a period of material expansion, followed by a period of financial expansion, elaborating differences and similarities of each cycle, over time. During material expansions, the world capitalist economy grows on a stable path, dominated by productive activity. The path is eventually disrupted by the surfacing of underlying contradictions. The most important of these contradictions is intensifying competition among capitalists and/or core capitalist states. The cycle then shifts to financial expansion, a period of crisis, chaos, and restructuring, in which speculative activity takes precedence over productive activity.

Arrighi’s formulation of systemic cycles of accumulation, like the work of Samir Amin, Immanuel Wallerstein, Andre Gunder Frank, and other world historical thinkers, is an effort to update, historicize, and build on insights of Vladimir Lenin, Rosa Luxemburg, and other Marxist theorists of imperialism. For world historical thinkers, explanations of change in world capitalism provided by Marxist theorists are limited by their tendency to center explanations on shifts within Europe, most often in the late 19th century. The project of world historical theorists is to account for time, space, and hierarchies of power, including in the Majority World (i.e., Africa, Asia, Latin America, the Caribbean, and the Pacific Islands), from 1492. The arrival of Europeans in what is now known as “the Americas” is argued to have marked the beginning of a series of transformations, leading to what we know today as “the world economy.” 3

Of greatest concern here is the fourth (US) systemic cycle, the material expansion of which reached its height in the period of 1950 to 1970. Arrighi (1994, 239–240) argues that “the internalization of transaction costs” is the distinct feature of the fourth systemic cycle of accumulation. In some detail, beginning around the 1880s, US business enterprises were the first to combine activities and transactions previously carried out by separate business units. This both reduced, and made more calculable, transaction costs. Enterprises thus expanded control, and in turn profits, through vertically integrating the long chain of activities extending from primary production to final consumption. Vertically integrated firms arose not only in manufacturing industries, but also in retail, for example, the rise of mass marketers that came to control a range of activities from retail shops to advertising, mail order houses, and chain stores.

By the early 20th century, vertically integrated firms had “become a source of permanence, power and continued growth” (Chandler 1977; as cited by Arrighi 1994, 241–242). Henceforth they became “multinational”—a term that would emerge much later—expanding beyond the US market, first in the rest of the Americas, then in Western Europe. Following the destruction caused during World War II, US multinational corporations (MNCs) rose to greater power and prominence in the rebuilding of Europe, creating intensified demand for a range of raw materials produced in Africa and the rest of the Majority World. This demand was compounded by that of the zaibatsu of Japan, that were similarly rebuilding Japan and other parts of East Asia (Valiani 2002).

With the intensification of activity and accumulation by US firms in Western Europe in the 1950s, US firms began banking in Western Europe, rather than in the US, in the Eurodollar markets that had sprung from the need of Warsaw Pact states to store US-denominated foreign exchange outside of the US (Arrighi 1994; Amin 1995). By the early 1960s, New York banks, which had joined US multinationals in the Eurodollar market, came to dominate 50 percent of the market, creating, by the late 1960s, an explosion of liquid funds beyond the control of states, including the US (Arrighi 1994, 300–301). Adding to this liquidity explosion were the Petrodollars generated by the seizure of control of the oil supply by oil-rich countries, in the early 1970s. Though today a normalized feature of international finance, this was the start of offshore banking and the speculative booms typical of financial expansions in systemic cycles of accumulation.

No longer able to control the global flow and generation of US dollars through the Federal Reserve, the US state was forced, in 1971, to abandon the dollar–gold exchange standard. With the adoption of a pure dollar standard and floating exchange rates, in 1973, the US was able to release unlimited quantities of non-convertible dollars into global circulation, thereby fueling further the liquidity explosion between 1973 and 1978 (Arrighi 1994, 308). Amin (1995) notes this may be seen as the end of the Bretton Woods mandate, with the IMF already having failed to maintain stability of world financial flows, despite the creation of Special Drawing Rights in the 1960s. Amidst the liquidity boom and financial chaos which also created inflation, when an ensemble of European countries, the Group of Ten, tried to use the Bank of England to impose regulations on banks operating in the Euromarket, banks simply moved further offshore, many to bases in the former colonies of Britain.

African Elites in the Fourth (US) Systemic Cycle of Accumulation

Though investing a wealth of intellectual, planning, and state resources in import substitution policies from the 1950s to 1970s, newly independent African states—regardless of ideological sympathies—remained dependent on raw material exports. To feed import substitution, African states and burgeoning national bourgeoisies imported technology, largely produced by the same multinational, vertically integrated firms discussed above. This strategy of creating domestically oriented economies was costly, both in terms of licenses and other rents charged by MNCs, and foreign exchange (Valiani 2012). For the most part, African states and capitalists failed to question the notion of “catching up” in processes of industrialization that had begun in very different conditions, in Europe and North America, several decades before. Like most states and capitalists of the time, African elites fell into the belief that the boom of “the Golden Age” would continue indefinitely, and ongoing demand for African raw materials would allow for the inflow of required foreign exchange. The spate of nationalizations—mainly of mining operations—that was carried out by African and other Majority World states during the 1970s, added to these foreign exchange requirements (Valiani 2002).

Bienefeld (2000, 538–539) paints a picture of the atmosphere in which African and other states took the cheap loans available in the booming, speculative frenzy of the 1970s:

. . . even public officials acting purely in the public interest, as they perceived it, would have had great difficulty justifying their refusal to accept such financial resources. The obvious short term benefits of such inflows; the euphoria that thrives in such speculative periods; the arrogant and myopic confidence that emanates from the ubiquitous “financial experts” who are also getting rich in the process; together these would always threaten to overwhelm any prudent officials seeking to limit their government’s exposure to risk. In fact, such people will tend to be replaced by those who are only too willing to play the game, to mouth the speculator’s platitudes and promises and to denounce them as “backward looking” people who fail to understand that the old rules no longer apply in “the new economy.”

Though interest rates were low due to the great world supply of mobile US dollars, the credit on offer was high risk at floating exchange rates. African and other primary commodity-supplying states were in need of foreign exchange—yet greater need than previously—due to the range of instabilities caused by floating exchange rates, including on exports, imports, government revenue, and national income.

With the raising of US interest rates in October 1979, popularized as the Volker shock, loans taken by states at very low-interest rates became unserviceable, and the rest of the story is fairly well known. In brief, the IMF was retooled with the function of managing capitalist structural reforms in indebted countries of the Majority World. Adebayo Olukushi (2021) speaks of IMF officials appearing in government quarters throughout Africa, selling the need to “adjust,” a sensible sounding term with which state officials found it difficult to argue. As Bienefeld (2000) points out, however, part of all structural adjustment programs was new loans. This is because it was well understood that in addition to loan repayment, the IMF prescription would create new foreign exchange shortages.

Arrighi (1994, 319) underlines the US’s 1979 move to restrict US money supply as a turning point. Having allowed financial capital to flow unregulated for most of the 1970s, the US elected to cooperate with the world’s largest financial capitalists, despite the known, detrimental impact of high interest rates on production and employment. Arrighi insists this was a choice made by the most powerful classes of the US elite, not a misgiving of economic theory or policy.

Similarly, the agency of African elites, in the 1980s, must be rigorously examined. Why, for instance, was President Thomas Sankara’s “Front uni d’Addis-Abeba contre la dette” (Addis Ababa United Front against the debt) a lone call at the Organization of African Unity Summit of 1987? 4 By this time, as elaborated above, it was both well known, and openly discussed, that international banks had been brought back to solvency, and better, following the first few years of structural adjustment. In 1985, the World Bank had acknowledged that private banks had used their leverage to pressure distressed borrowers into providing public guarantees for loans whose commercial viability they claimed to have assessed, but essentially stopped assessing, once public guarantees had been put in place (World Bank 1985, 114; as cited by Bienefeld 2000, 538). Further, the choice to insist on full repayment of loans had been made by the US and the rest of the G7 in the absence of international law applying to the situation (Bienefeld 2000). Through this maneuver of core capitalist states, creditors were exonerated for making high-risk loans, and debtors assumed to be responsible for all costs.

Put succinctly, in what would be the last of Sankara’s major political stances, the Burkina Faso President was proposing to African states the strategy of a debtor’s cartel to counter the Paris Club, the cartel of lenders, backed by core capitalist states, in a policy space uncharted by international law. That this strategy was not a consideration for more African leaders is yet more questionable given that, by this time, the World Bank was openly stating, for instance in its “World Development Report,” that the lending boom of the 1970s was “evidence that even competitive financial markets can make mistakes” (World Bank 1989, 4).

Indirectly, and without necessarily intending to, Ndongo Samba Sylla (2020) provides part of the answer to the question of the agency of African elites. Sylla makes a distinction between two types of indebted African states: those earning enough foreign exchange through trade to keep up with debt servicing, and those unable to generate trade surpluses which attempt to draw in foreign exchange through foreign direct investment (FDI). Sylla points out that foreign exchange is far more crucial to African countries than to indebted wealthy countries because the debt of the latter is not in foreign currencies, for instance, Japan, the country with the highest debt in the world.

For those African states able to service debts, most often those exporting oil and other high-value minerals, when world prices of these raw materials increase, states tend to take on more debt, which according to Sylla (2020), ushers in more austerity. For those states seeking to draw in foreign exchange through FDI, when successful, such investment leads to more pressure on foreign exchange supply given profit repatriation, increased need to import technology, and high wages of imported experts. Here Sylla (2020) gives the example of Senegal, with a trade balance that has been in structural deficit since 1967. For Senegal and other countries using the CFA franc, 5 the situation is worsened by the inability of central banks to issue currency. The “only option” left for such countries is to “maintain the trust” of donors by implementing orthodox fiscal policy that is “discriminatory” in that it puts foreign debt service before domestic debt payment and investment in social programs and public services (Sylla 2020).

Sylla makes the link to capital flight, but attributes it only to foreign investors. Sylla explains that through “accounting tricks,” foreign investors make illicit transfers and these lower the value of national currencies, thus increasing the value of debt and aggravating balance of payments deficits. Meanwhile, the cost of imported manufactures and other imports needed by indebted states tends to rise, further feeding foreign exchange shortages. Sylla then draws the analogy of a Ponzi scheme:

In financial parlance, a Ponzi scheme is a type of scam consisting of paying interest payments due to investors (in our case the service on ongoing debt) with money obtained from new investors attracted by the prospect of high earnings (in our case the issuance of new debt). (Sylla 2020)

Sylla’s conclusion is that Senegal has “innocently” employed “this strategy” since 1960. His view of African officials as innocent is not unlike Olukushi’s stated above: that African officials were and continue to be powerless, with little agency. Similarly, Sylla underlines foreign investors as the main actors responsible for capital flight.

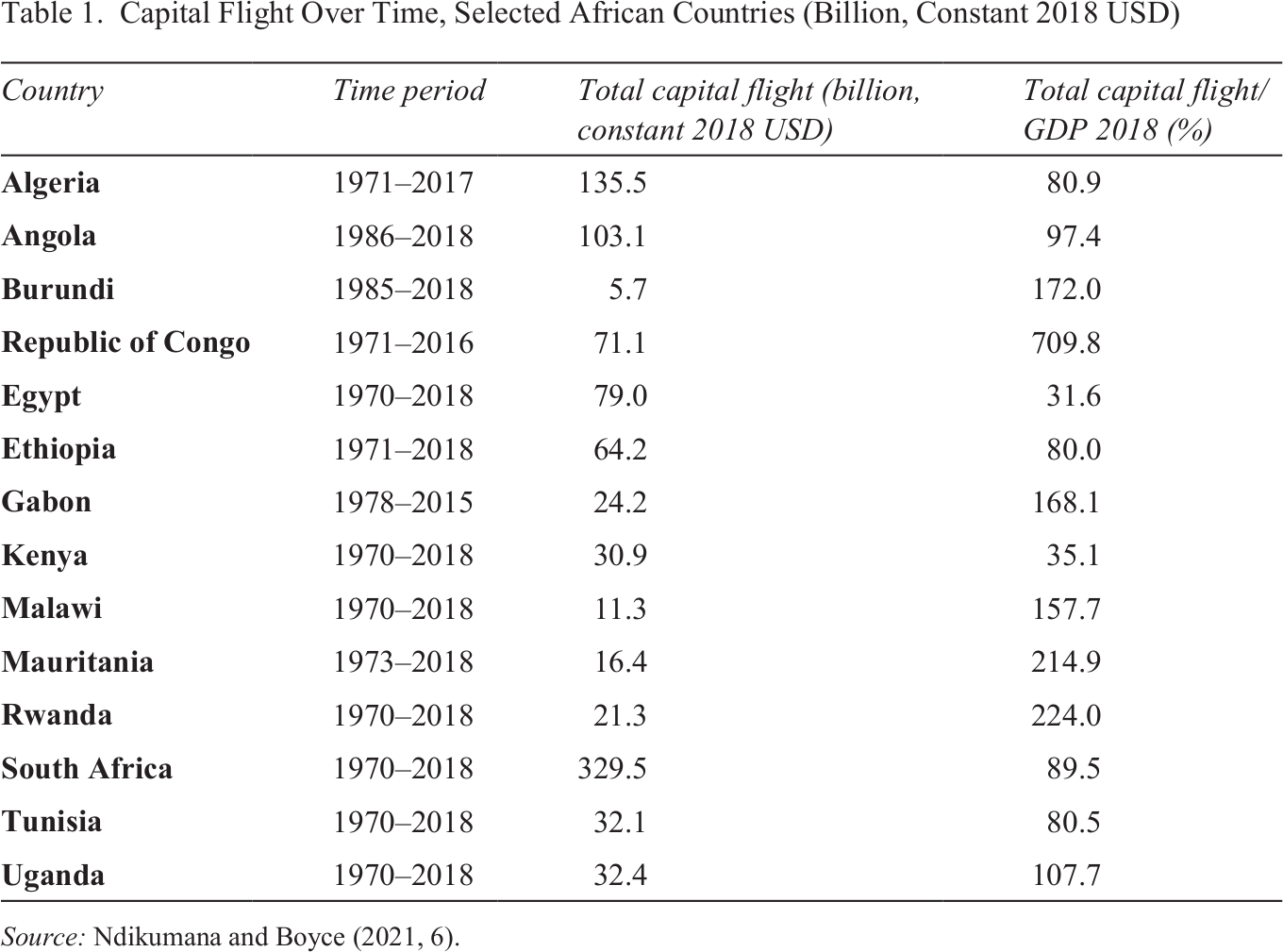

To be clear, it is not only foreign investors, but also African capitalists and officials that are engaged in capital flight. A sampling of Ndikumana and Boyce’s (2021) estimates shows the range of figures, over time, for countries in both of Sylla’s categories (major raw material exporters and FDI-dependent), as well as countries falling outside Sylla’s categories (see Table 1).

Capital Flight Over Time, Selected African Countries (Billion, Constant 2018 USD)

Source: Ndikumana and Boyce (2021, 6).

Ndikumana and Boyce specify that trade misinvoicing occurs in the export of oil, minerals, and agricultural goods, to the tune of some 1 trillion USD between 1970 and 2018. Some misinvoicing also occurs through the under-invoicing of imports to avoid import tariffs, amounting to some 505 billion USD in the continent between 1970 and 2018. The co-authors note this is “facilitated by the complicity of a complex network of actors and exacerbated by poor governance in host countries” (Ndikumana and Boyce 2021, 5).

In a paper on capital flight focusing on Angola, Côte d’Ivoire, and South Africa, from the 1970s, Ndikumana and Boyce state “the fact that these outflows have persisted over a long period indicates that they are driven by fundamental structural and institutional factors pertaining to both the source countries and the global financial system.” The authors state further that, “these outflows have led to the accumulation of massive offshore wealth belonging to the economic and political elites from these countries, even as their populations continue to face deprivation in access to basic services” (Ndikumana and Boyce 2019, i).

Comparing income inequality within African countries with similar data from other world regions and large countries, Chancel and others (2019, 2) find the largest gaps in Africa. Pre-tax income held by the richest 10 percent of African country populations ranges from 37 percent in Algeria, to 67 percent in Botswana, while pre-tax income held by the bottom 50 percent is at most 14 percent in Algeria, and as little as 4 percent in South Africa. Overall, the top 10 percent in Africa is six times richer than the bottom 50 percent. This compares with factors of 2.5 in Russia, 2.8 in China, 3.4 in the US, 3.7 in India, and 4.0 in Brazil and West Asia.

Amin explicitly addresses the agency of African elites in this configuration. He argues that after the 1975 rejection by rich countries of the Non-Aligned Movement’s New International Economic Order (NIEO), instead of questioning the potential of capitalism to serve the majority, African elites and those of other states of the Majority World, shifted from a national bourgeois vision of capitalist development to a comprador bourgeois vision (Amin 1995, 29).

The NIEO, more widely known as the Bandung proposals, was largely centered on reforming world capitalism to make room for capitalists producing manufactured goods in the Majority World. Among others, the NIEO included recommendations around opening core markets to Majority World industrial exports, reducing the cost of technology transfer from the core to the Majority World, and improving the terms of trade for agricultural and mineral exports. Continued export of agricultural and mineral raw materials was an important part of the national bourgeois development vision because, as alluded to earlier, import substitution was not imagined beyond emulating manufactures and methods devised in the core, and these require high levels of foreign exchange.

To recall analytical tools rarely used today, but that originated in critical African political economy discussions from the 1950s, a national bourgeois vision aims to develop domestically oriented economies along capitalist lines, primarily led by nationally based capitalists. The comprador bourgeois vision centers on raw material exports, foreign capital, and domestic capitalists active mainly in international trade and local retail activity. 6 Amin (1995, 29) notes this elite choice was reinforced by the rise of a new, privileged middle class during the immediate post-independence period of bourgeois national capitalist development. The interests of this new privileged class varied significantly from those of the majority.

Some 25 years later, Amin makes the systemic link between Majority World elite choices and world financial expansion:

The breathtaking growth in financial investments requires—and sustains—among other things, the growth in the debt, in all its forms, particularly sovereign debt. When existing governments claim to pursue the goal of “debt reduction,” they deliberately lie. The strategy of financialized monopolies needs growth in the debt (which they seek and do not oppose)—a financially attractive means to absorb the surplus from monopoly rents. Austerity policies imposed to “reduce the debt,” as it is said, actually end up increasing its volume, which is the sought-after consequence. (Amin 2019, 33)

Building on Amin and other world historical analyses for the current discussion, by the early 1980s, African states and capitalists had essentially abandoned the aim of achieving economic independence for the benefit of the majority. Instead, they chose to fortify the world capitalist structure through a new form of comprador bourgeois capitalism, the basis of which consists of a) foreign capital that takes a variety of forms, the major ones being foreign credit (including that taken as public loans), foreign direct investment, foreign aid from states, and private foreign aid via nongovernmental organizations and foundations; and b) the use of public resources, of unprecedented magnitude, including public loans, to support local as well as international capitalists engaging in a range of accumulation and profit-making activities.

Bunevich and co-authors (2019) offer an analytical tool that complements the structural, world historical approach to understand contemporary elite agency in indebted countries of not only Africa, but also Asia, and the former Warsaw Pact. They argue that external debt becomes a state interest when the attraction of new credit becomes central to the interests of a dominant class, group, family, clan and/or religious elite. Lobbying, public programs, and policy development thus become driven by the goal of accumulating loaned funds, leading the nation into a “debt pit” (Bunevich et al. 2019, 52).

Incorporating this analytical tool, Africa’s status as a net creditor to the world is of yet greater weight and systemic importance than what is implied in Ndikumana and Boyce’s numerical comparison of total debt owed to the stock of wealth resulting from capital flight—a ratio of 0.36, by 2018. In failing to challenge the G7’s approach to loan repayment as one not based in international law, in the early to mid-1980s; in implementing IMF prescriptions and comprador bourgeois-oriented reforms through the decade; and in using their power, as public officials, to continue borrowing from a range of international sources, amassing some 720 billion USD in public debt by 2018—African states have fed global financial expansion with immeasurable consequence for the continent. That Africa is a major locus for the perpetuation of liberalized world trade and financial flows is borne out by the fact that the continent’s external debt has now surpassed, in nominal terms, the 900 billion USD debt incurred, in the 1970s, by Africa, Asia and Latin America combined. While being instrumental in this process, African elites—both public officials and capitalists (often one and the same individuals)—have benefited, as a class, as demonstrated by capital flight estimates and releases like the Pandora Papers. In sum, comprador bourgeois capitalism, in its new form, is the African expression of financial expansion in the fourth (US) systemic cycle of accumulation of historical capitalism.

Policy Tendencies of Comprador Bourgeois Capitalism in 21st-Century Africa

This section sketches the contours of major policy tendencies of 21st-century comprador bourgeois capitalism in Africa at two levels: the macro and micro. Using illustrations from certain countries of the continent, the sketch is by no means complete. Rather, it proposes a framing that may be used to understand, with greater depth and connection, the systemic causes and particular policy experiences in the diversity of countries that form the African continent.

The first policy contour, at the macro, and arguably, most basic level, is continuous austerity, rationalized and implemented by elites throughout the continent, regardless of the degree of state indebtedness. An example of this, of widespread human consequence, is in the area of healthcare. During the last major pandemic in Africa, in the 2001 Abuja Declaration on HIV/AIDS, Tuberculosis, and Other Related Infectious Diseases, African states committed to a healthcare spending target of 15 percent of general government expenditure. Taking average government health expenditure between 2002 and 2019 (latest available WHO data), as compiled in “The Africa Care Economy Index” (Valiani 2022; WHO 2021), not a single African state met this target. Average healthcare spending for the period ranges from the extreme low of 1.9 percent in Equatorial Guinea, to 13.8 percent in South Africa.

Given high levels of illness and disability throughout the continent, and the dominant role of unpaid female labor in caring work, investment in public healthcare is vital to supporting the majority in Africa, including women and girls. The failure of states to meet the healthcare spending target to which they committed, albeit minimal, and set arbitrarily rather than based on need, translates to the reintensified exploitation of female caring labor. The reintensification of exploitation of female caring labor is a feature of the current global financial expansion identified by Valiani (2012), in varying forms, for the indebted Philippines, as well as for two core countries, the US and Canada.

The implementation and perpetuation of so-called social protection grants, by African states, is another macro-level policy typical of the new comprador bourgeois capitalism in the continent. These means-tested grants, well below survival levels, are often linked to new loans taken by African states, along with commitments to deepened capitalist reform. The Takaful and Karama Cash Transfer Program of Egypt is one example. In 2015, Egypt’s Ministry of Social Solidarity started the program, on the basis of a $400 million World Bank loan, providing conditional and unconditional grants to extremely impoverished, largely female-headed households. Cash transfers range from monthly amounts of 325 to 605 Egyptian pounds (EGP), with maximum support for three children, which is below the average fertility rate. In contrast, one living wage estimate calculates 3,957 EGP for an average family in rural Egypt in 2020 (Global Living Wage Coalition 2020). The Takaful and Karama Cash Transfer Program is part of “an ambitious economic reform program,” as described by the World Bank (2018), that includes the removal of energy subsidies, the adoption of a flexible exchange rate and the introduction of a new value-added tax.

Payment of “social protection” grants is often attached to culturally specific financial instruments, for example, funeral insurance for extended family. In an article titled “Insecurity in South African Social Security: An Examination of Social Grant Deductions, Cancellations, and Waiting,” Natasha Vally (2016) examines this for the instance of South Africa, showing how financial instruments are tied to grants, both with and without the consent of recipients. More broadly, culturally adjusted financial instruments, largely peddled by South African banks and targeted to middle classes, may be found in several countries of Southern Africa.

At the micro level, 21st-century comprador bourgeois capitalism tends toward policies facilitating intensified production and export of primary products. From the 2000s, African states throughout the continent have enabled the sale of large tracts of customary shared land to foreign investors and states. Among others, these land sales have been documented in Uganda, Tanzania, Madagascar, Somalia, Ethiopia, Nigeria, Ghana, Sao Tome and Principe, and Liberia (Alter 2013; Chung and Gagné 2021). Whether sales transactions have materialized in all instances or not, this round of land dispossession has been driven by state interests in increasing cash crop and raw material production for export to generate foreign exchange required for continued borrowing in international credit markets.

Along the same lines, for the past few decades, African states have been making marine fishing agreements with European states, a sector now valued at 24 billion USD per year. Issuing licenses and developing regulations to support the needs of industrial scale, international fishing companies have been the focus of African states, despite the known higher incidence of illegal and unreported fishing in industrial fisheries, as compared to small-scale fisheries (Okafor-Yarwood et al. 2020).

Ecological degradation resulting from this intensified land and water-based extraction is deepening the degradation that was already in process during the colonial and immediate, post-Independence periods. This has implications for laborers, work, and social reproduction. In the cocoa export-driven Ivory Coast, for instance, over the past two to three decades, with a dwindling supply of forest land to clear for the cultivation of cocoa, previously planted land is being re-cultivated. This is a highly labor-intensive process, the cost of which is not covered by multinational-controlled, world cocoa prices. As in neighboring cocoa-exporting countries, highly exploited, migrant adult laborers in the Ivory Coast have been replaced with highly exploited, migrant children (Odijie 2020). The social fallout of such production is, in turn, carried by women and girls, adding to the already heavy burden of malnutrition, food insecurity, and under-funded public healthcare. Over 10 percent of the 22.7 million Ivory Coast population was facing food insecurity in 2020, and 21 percent of children under five were chronically malnourished (Action Against Hunger 2021). Similarly, the social fallout of super-exploitation in cocoa production is carried by the predominantly female caregivers of migrant child workers.

Bringing together macro- and micro-level tendencies of comprador bourgeois capitalism in Africa is the little-known story of COVID-19 vaccine development at the African Centre for Excellence in Genomics and Infectious Diseases (ACEGID), in Nigeria. As early as September 2020, the ACEGID had completed pre-clinical trials for a vaccine showing over 90 percent effectiveness against the first and second variants of the novel coronavirus. In order to facilitate distribution in Africa and other parts of Majority World, the ACEGID elected not to patent the vaccine. 7 The ACEGID, however, was not able to pursue clinical trials for its promising vaccine because it failed to obtain support from the African Union and wealthier African states that it approached. The amount required for clinical trials was 250 million USD. Around the same time, African states, via the African Union, pooled public resources as collateral for a 2 billion USD loan from the Africa Export Import Bank (AFREXIMBANK). The loan was for the purpose of supporting clinical trials in Africa of COVID-19 vaccines produced elsewhere—in the main, vaccines produced by the world’s major pharmaceutical firms ( Quartz Africa 2021; Valiani 2021b).

Headquartered in Cairo, and listed on the Stock Exchange of Mauritius, the AFREXIMBANK has offices in Abidjan, Harare, Abuja, and Kampala. Its investors are African governments, African central banks, African private banks, international private banks and financial institutions, and wealthy individuals. 8 Established in 1993 to funnel public and other resources toward the activity implied in its name, the AFREXIMBANK is a hallmark of 21st-century comprador bourgeois capitalism in the continent.

Conclusion

In 1995, a decade after the so-called “third world debt crisis,” Samir Amin foresaw what he colloquially termed “the fourth worldization” of Africa. It is argued here that both elites of the capitalist core countries, and elites of Africa, opened the path of this fourth worldization, creating the conditions for Africa to become a major locus for the maintenance of liberalized world financial and trade flows.

In detail, this study demonstrates how, circa 1980, following the Volker shock, African elites took a central role in this path-making by shifting states from the aim of economic independence to a new form of comprador bourgeois capitalism. In so doing, African elites have fortified the financial expansion of the fourth (US) systemic cycle of accumulation, while benefiting as a class, through the debt pit and private accumulation via capital flight. The new comprador bourgeois capitalism is argued to be the African expression of global financial expansion in the fourth (US) systemic cycle of accumulation. It is characterized by a) foreign capital that takes a variety of forms, the major one being foreign credit taken as public loans; and b) the use of public resources, of unprecedented magnitude, including public loans, to support local as well as international capitalists in a range of profit-making activities, including investment and savings via offshore accounts.

Major policy contours of the new comprador bourgeois development are also offered, though far from an exhaustive recounting. Links are drawn between the deliberate perpetuation of public indebtedness and a) austerity and the intensified exploitation of female caring labor, b) so-called social protection grants, and implementation of new financial instruments, c) intensified export-oriented production of raw materials and cash crops and deepening socio-ecological degradation, and d) supporting the spread of MNC health technology to the detriment of non-commodified, non-profit health technology production in Africa.

In closing, it is proposed that building on the world systemic analysis presented here, in-depth national and (sub)regional explorations, in and beyond Africa, could specify the class and other dynamics of the debt pit, concretizing these histories and making them more tangible. A composite of such understandings could create a historically and space-specific tableau, from which a plurality of political agendas could be constructed with a vision of shifting the world toward humane rebeginnings.